How I Prepared for My Newborn Without Breaking the Bank – A Real Parent’s System

When I found out we were expecting, excitement quickly turned into stress—how would we afford a baby without derailing our financial future? Like many parents, I feared hidden costs and overspending. But instead of panicking, I built a system. Not a rigid budget, but a flexible, realistic plan focused on control, clarity, and calm. Here’s how I tackled newborn preparation not with perfect savings, but with smart, sustainable cost control that actually works.

The Reality Check: Facing the True Cost of a Newborn

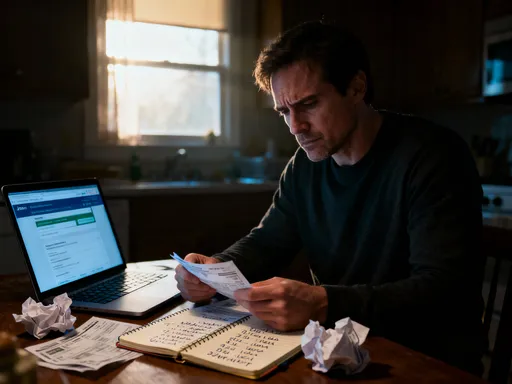

The arrival of a newborn brings joy, but it also introduces a wave of financial pressure that many families are unprepared for. While the emotional journey is widely discussed, the financial reality often catches parents off guard. From prenatal visits and delivery fees to car seats, diapers, and nursery furniture, the expenses add up quickly. According to widely cited estimates, the average cost of raising a child in the United States exceeds $300,000 from birth to age 17, not including college. While that number may feel overwhelming, it’s important to remember that much of that cost accumulates over time. The real challenge lies in managing the initial surge of newborn-related spending without compromising long-term financial stability.

Many expectant parents underestimate the true scope of early baby expenses because they focus only on visible items like strollers or cribs, overlooking recurring costs such as diapers, formula, and medical co-pays. Others assume everything must be new, leading to unnecessary spending. For example, a high-end stroller can cost over $800, while a safe, functional model is available for under $200. Similarly, baby clothing is often worn only a few times before outgrowing it, making expensive designer outfits a poor value. The gap between expectation and reality becomes clear when families face surprise medical bills or realize they’ve spent hundreds on items their baby rarely used.

Emotional decision-making plays a major role in early spending. Retailers and advertisers capitalize on parental love and anxiety, promoting the idea that spending more equals better care. This mindset can lead to overbuying and financial strain. The first step toward financial control is awareness—recognizing that preparation doesn’t require perfection or extravagance. By acknowledging the true cost landscape, parents can shift from reactive spending to intentional planning. This mindset change is not about deprivation, but about empowerment. When you understand what you’re actually paying for, you can make choices that align with both your values and your budget.

One of the most effective tools in this phase is creating a preliminary expense list. This includes one-time purchases like a crib or car seat, recurring costs like diapers and wipes, and potential medical expenses not fully covered by insurance. By listing these items early, parents gain visibility into their financial roadmap. This process also helps identify areas where costs can be reduced without risk to the baby’s safety or well-being. The goal is not to eliminate spending, but to make it deliberate and informed. Awareness transforms fear into action, laying the foundation for a structured, stress-reducing financial plan.

Building Your Financial Foundation Before Day One

Before welcoming a newborn, it’s essential to assess your current financial situation with honesty and clarity. This step goes beyond tallying bank balances—it involves understanding cash flow, identifying fixed and variable expenses, and preparing for income changes during maternity or paternity leave. Many families experience a temporary reduction in income during the first few months after birth, especially if one parent takes unpaid leave. Planning for this shift is critical to avoid dipping into emergency funds or accumulating debt.

A key part of this preparation is reviewing your household budget with the baby in mind. Start by mapping out your monthly income and all current obligations, including housing, utilities, debt payments, and groceries. Then, estimate the additional costs associated with the newborn. This includes both predictable expenses like diapers and formula and potential surprises like specialized medical care or lactation support. Once you have a clearer picture, adjust your spending in advance. For example, reducing discretionary spending on dining out or subscriptions can free up hundreds per month, creating breathing room before the baby arrives.

Equally important is building or reinforcing an emergency fund. Financial experts often recommend having three to six months’ worth of living expenses saved, but for new parents, an additional buffer may be wise. Unexpected situations—such as a premature birth, extended hospital stay, or complications requiring specialized care—can lead to significant out-of-pocket costs. Having a dedicated “baby emergency” fund, even if it starts small, provides peace of mind. This fund doesn’t need to be fully stocked before delivery; setting a target and automating small monthly contributions can steadily build it over time.

Another crucial element is income planning during parental leave. If your employer offers paid leave, understand the duration and amount. If not, explore options like short-term disability insurance, which may cover part of your income during maternity leave. Some families also consider temporary side income opportunities, such as freelance work or selling unused items, to offset lost wages. The goal is to create a realistic income projection for the first three to six months postpartum and align your spending accordingly. This proactive approach prevents last-minute financial scrambles and supports a smoother transition into parenthood.

Smart Spending: Distinguishing Needs from Wants in Baby Gear

One of the most effective ways to save money while preparing for a newborn is learning to distinguish between essential items and optional luxuries. Many baby products are marketed as must-haves, but in reality, only a few are truly necessary for the first few months. A safe crib or bassinet, a reliable car seat, diapers, wipes, and basic clothing are the core needs. Everything else—designer outfits, high-tech monitors, or multiple nursery decorations—falls into the “nice to have” category. By focusing on essentials, parents can avoid overspending on items that offer little practical benefit.

Buying gently used items is one of the smartest financial decisions new parents can make. Babies grow quickly, and many products are barely used before they’re outgrown. Secondhand markets, online parenting groups, and local consignment stores offer high-quality baby gear at a fraction of retail prices. Cribs, strollers, swings, and clothing are often available in excellent condition. When purchasing used items, safety is paramount. Always check for product recalls, ensure the item meets current safety standards, and avoid used car seats or cribs with unknown histories, as these can pose risks. For other items, such as clothing or toys, gently used is perfectly safe and economical.

Hand-me-downs from friends or family members are another valuable resource. Not only do they save money, but they also strengthen community ties and reduce waste. Many parents find that receiving a box of baby clothes or a nearly new stroller feels like a gift of support. When accepting hand-me-downs, be selective—take only what you’ll actually use and ensure everything is clean and in good condition. At the same time, don’t feel obligated to accept everything offered. Being polite but clear about your needs helps maintain healthy boundaries while still benefiting from generosity.

Another key strategy is choosing versatile, durable products over trendy or single-use items. For example, a convertible car seat that grows with the child may have a higher upfront cost but saves money over time by eliminating the need for multiple seats. Similarly, a simple wooden crib that can convert into a toddler bed offers long-term value. When it comes to clothing, opting for neutral colors and simple designs allows for mix-and-match use across seasons and hand-me-downs to siblings or friends. These choices reflect a mindset of sustainability and practicality, reducing both financial and environmental costs.

Healthcare Planning: Navigating Insurance and Medical Costs

Medical expenses are among the most significant and unpredictable costs associated with a newborn. Even with health insurance, families can face substantial out-of-pocket charges for prenatal care, delivery, postnatal visits, and newborn screenings. The key to minimizing financial stress is proactive insurance planning. This begins with a thorough review of your current health plan, including coverage limits, co-pays, deductibles, and out-of-pocket maximums. Understanding these details helps you anticipate costs and avoid surprise bills.

One of the first steps is confirming that your chosen hospital, obstetrician, and pediatrician are in-network. Out-of-network providers can result in significantly higher charges, sometimes amounting to thousands of dollars in unexpected costs. Contact your insurance provider directly to verify coverage and request a detailed estimate of expected expenses for delivery and newborn care. Some hospitals offer financial counseling services to help patients understand their potential bills, which can be a valuable resource.

Another important tool is the Health Savings Account (HSA) or Flexible Spending Account (FSA), if available through your employer. These accounts allow you to set aside pre-tax dollars for qualified medical expenses, effectively reducing your taxable income while building a fund for baby-related costs. An HSA offers the added benefit of rolling over unused funds year to year, making it a powerful long-term savings vehicle. Contributions can be automated, ensuring consistent funding without relying on willpower. Using HSA or FSA funds for items like breast pumps, lactation consultants, or baby medications can lead to significant tax savings.

It’s also wise to plan for newborn-specific medical needs. Most hospitals require certain screenings and vaccinations shortly after birth, and some tests may not be fully covered. Additionally, complications such as jaundice or feeding difficulties may require follow-up visits or treatments. By discussing potential scenarios with your healthcare provider and understanding what your insurance covers, you can prepare financially for these possibilities. Some parents choose to set aside a specific amount—such as $1,000—in a dedicated medical fund to cover initial newborn care, providing a safety net without straining their overall budget.

Systematic Savings: Automating for Consistency, Not Perfection

One of the most effective financial habits new parents can adopt is automation. Relying on willpower to save money is unreliable, especially during the emotional and physically demanding period of pregnancy and early parenthood. Instead, setting up automatic transfers ensures consistent progress toward financial goals without requiring constant attention. This approach removes decision fatigue and builds momentum over time.

The first step is creating a dedicated savings account for baby-related expenses. This account should be separate from your regular checking or emergency fund to prevent accidental spending. Once established, set up automatic transfers from your primary account on payday. Even small amounts—such as $50 or $100 per paycheck—can add up significantly over several months. The key is consistency, not the size of the contribution. Over a year, $100 every two weeks amounts to $2,600, a substantial cushion for initial baby costs.

Automation can also be applied to debt repayment and retirement savings. If you’re paying off student loans or credit cards, maintaining or increasing automatic payments helps prevent debt from growing during periods of reduced income. Similarly, continuing retirement contributions, even at a slightly reduced rate, protects long-term financial health. Many employers offer automatic payroll deductions for retirement plans, making it easy to stay on track. The goal is to treat these savings and payments as non-negotiable expenses, just like rent or utilities.

Another benefit of automation is psychological. When savings happen automatically, you’re less likely to view the money as available for spending. This creates a mental barrier that supports disciplined financial behavior. Over time, automated systems become a normal part of your financial routine, reducing stress and increasing confidence. Parents who use this strategy often report feeling more in control, even when faced with unexpected costs. Automation turns intention into action, making financial preparation sustainable and manageable.

Long-Term Thinking: Aligning Newborn Costs with Family Financial Goals

Bringing a baby into the family is not just a short-term expense—it’s a long-term financial commitment that affects every aspect of your financial plan. Rather than treating baby costs as an isolated budget line, it’s more effective to integrate them into your overall financial strategy. This means revisiting your long-term goals, such as homeownership, retirement, and education savings, and adjusting them to reflect your new reality. The goal is balance: providing for your child today without sacrificing your family’s future security.

One way to achieve this balance is through intentional trade-offs. For example, delaying a home renovation or vacation to prioritize baby expenses is a responsible choice that maintains financial stability. Similarly, reducing contributions to a college fund temporarily while increasing baby-related savings is acceptable, as long as retirement savings remain on track. Financial experts often emphasize that parents should not sacrifice their own retirement to save for their children’s education, as retirement cannot be financed through loans.

Another important consideration is the opportunity cost of spending decisions. Every dollar spent on a luxury baby item is a dollar not saved for future needs. By evaluating purchases through this lens, parents can make more thoughtful choices. For instance, spending $500 on a high-end baby monitor might mean delaying a family emergency fund contribution or reducing investment growth over time. Viewing spending in the context of long-term impact encourages more deliberate decision-making.

Regular financial reviews—quarterly or semi-annually—help ensure that baby-related expenses remain aligned with broader goals. During these reviews, assess whether your budget still reflects your priorities, whether savings targets are being met, and whether any adjustments are needed. This ongoing process fosters financial agility and prevents small oversights from becoming larger problems. By treating financial planning as a dynamic, evolving practice, families can adapt confidently to changing needs while staying on course toward long-term security.

Staying in Control: Monitoring, Adjusting, and Avoiding Financial Burnout

Financial preparation for a newborn is not a one-time task but an ongoing process that requires attention, flexibility, and emotional resilience. Even the best plan will encounter unexpected challenges, from medical surprises to changes in income. The key to long-term success is not perfection, but adaptability. By treating your financial plan as a living system, you can make adjustments as needed without feeling defeated by setbacks.

Simple tracking methods can make a big difference. Using a budgeting app, spreadsheet, or even a notebook to record baby-related expenses helps maintain awareness and accountability. Tracking doesn’t need to be time-consuming—just a few minutes each week can keep you informed. When you see where money is going, you can identify patterns, celebrate progress, and catch overspending early. This visibility reduces anxiety and reinforces a sense of control.

Regular review routines are equally important. Schedule monthly or quarterly check-ins to assess your financial situation. Are you meeting your savings goals? Have unexpected costs arisen? Do your spending habits reflect your priorities? These questions help you stay aligned with your plan and make informed adjustments. For example, if you find that diaper costs are higher than expected, you might explore switching brands or using a subscription service for discounts. If income has increased, you might decide to boost your retirement contributions or build your emergency fund faster.

Finally, emotional well-being plays a crucial role in financial decision-making. Parenting is demanding, and financial stress can amplify feelings of overwhelm. It’s important to practice self-compassion and recognize that no plan is flawless. Celebrate small wins, such as sticking to a budget for a month or receiving a helpful hand-me-down. Share financial responsibilities with your partner, if applicable, to avoid burnout. Open, non-judgmental conversations about money can strengthen your relationship and create a united front in facing challenges.

Ultimately, the goal is not to eliminate all financial stress—some level is normal—but to manage it in a way that supports your family’s well-being. By combining practical strategies with emotional awareness, parents can navigate the financial journey of early parenthood with confidence and calm. Preparation, planning, and persistence create a foundation not just for raising a child, but for building a resilient, secure family future.