How I Survived a Job Loss with These Financial Tools

Losing my job last year hit harder than I expected—not just emotionally, but financially. I quickly realized I wasn’t prepared for an unemployment emergency. But instead of panicking, I turned to practical financial tools that actually worked. Some I’d overlooked for years, others were new discoveries. This is how I stabilized my situation, protected my savings, and stayed afloat—without falling into debt traps or risky bets. The experience taught me that financial resilience isn’t about having a high salary; it’s about having the right systems in place before crisis strikes. What I learned could help anyone facing sudden income loss regain control and move forward with confidence.

The Wake-Up Call: Facing Unemployment Head-On

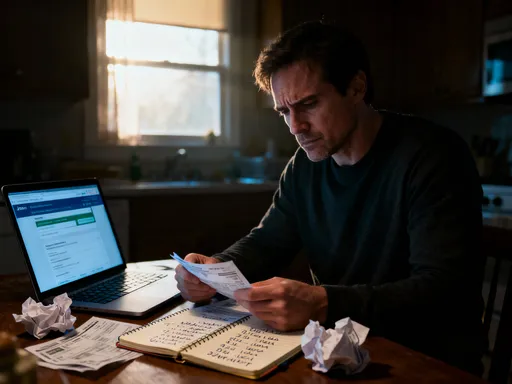

The call came on a Tuesday morning. I was told the department was being restructured, and my position was eliminated. There was no warning, no performance issues—just a polite goodbye and a severance package that felt generous until I calculated how long it would realistically last. Within days, the emotional toll began to match the financial strain. Sleep became erratic, and anxiety crept into every decision. The hardest realization wasn’t the loss of routine or identity, but the sudden stoppage of income. Rent, groceries, insurance, car payments—none of these paused just because my paycheck did.

What followed was a week of frantic assessments. I reviewed every bill, every subscription, every automatic withdrawal. I opened spreadsheets I hadn’t touched in months. The numbers didn’t lie: without intervention, my savings would last less than four months. That timeline shrank further when I factored in the psychological urge to spend—comfort purchases, impulse deliveries, the temptation to maintain appearances. I recognized that survival wouldn’t come from hope, but from structure. I needed tools that were not only effective but sustainable under pressure. This wasn’t about getting rich or chasing investment returns. It was about stability, clarity, and protecting what I already had.

The turning point came when I stopped viewing the situation as a personal failure and started treating it as a financial emergency requiring a disciplined response. I reminded myself that job loss is a common experience, not a reflection of worth. According to labor statistics, millions of workers face temporary unemployment each year, often through no fault of their own. The difference between those who recover quickly and those who spiral into long-term hardship often comes down to preparation and response. I decided I would not be among those who let panic dictate my choices. Instead, I committed to a methodical approach—using tools that were accessible, reliable, and grounded in real-world practicality.

Emergency Fund: The First Line of Defense

When my income stopped, the first thing that kept me from immediate crisis was my emergency fund. I had built it slowly over years, setting aside a small portion of each paycheck. At the time, it felt like an invisible safety net—something I hoped I’d never need. But when the layoff happened, that fund became the foundation of my financial survival. It covered rent for two months, groceries, and essential utilities while I navigated the next steps. Without it, I would have been forced to rely on credit cards or loans within the first week, setting off a chain reaction of debt that could have taken years to undo.

An emergency fund is not just savings—it’s strategic liquidity. It must be held in a safe, accessible account, separate from everyday checking or long-term investments. The goal is immediate availability without penalty or market risk. For most households, a reserve covering three to six months of essential expenses is a realistic target. This doesn’t mean luxury spending or discretionary travel—it means housing, food, insurance, transportation, and basic utilities. The exact amount varies, but the principle remains the same: when income stops, this fund keeps the lights on.

Yet many people make critical mistakes with their emergency reserves. Some keep the money in a regular savings account, where it’s too easy to dip into for non-emergencies. Others invest it in stocks or mutual funds, exposing it to market volatility. Still others save too little, believing they can rely on credit if needed. These missteps weaken the very purpose of the fund. I learned this the hard way when I once considered using part of my emergency savings to cover a home renovation. Thank goodness I didn’t—months later, that same fund was all that stood between stability and financial freefall.

The psychological benefit of having an emergency fund cannot be overstated. It provides breathing room. It reduces the pressure to accept the first job offer, no matter how poorly it pays or how misaligned it is with long-term goals. It allows time to think, plan, and act with clarity. For women in households where financial responsibility often falls heavily on their shoulders, this buffer is especially vital. It’s not just about money—it’s about autonomy, dignity, and the ability to make choices rather than react to crises.

Budgeting Under Pressure: Stretching Every Dollar

Once the initial shock wore off, I knew I had to take control of my spending. I created a crisis budget—one that reflected reality, not habit. This wasn’t about cutting out coffee or skipping the occasional dinner out. It was about a complete reevaluation of every expense. I categorized everything into three groups: essentials, deferrable costs, and non-essentials. Essentials included rent, utilities, groceries, and health insurance. Deferrable costs were things like car maintenance, subscription services, and credit card payments that could be negotiated or paused. Non-essentials—dining out, entertainment, new clothing—were suspended entirely.

One of the most effective changes was renegotiating recurring bills. I called my internet provider and asked for a retention discount. I switched to a lower mobile plan and canceled premium streaming services. I contacted my insurance agent to review my policy and found I was overinsured for my current needs. These adjustments saved over $200 per month—a significant amount when every dollar counts. I also started meal planning rigorously, buying in bulk, and using grocery store loyalty programs. By focusing on unit prices and shopping with a list, I reduced my weekly food spending by nearly 30% without sacrificing nutrition.

Another key strategy was timing. I aligned my bill payments with the days I received any incoming funds, even if they were small. This prevented late fees and maintained my credit standing. I used a simple spreadsheet to track every transaction, which helped me stay accountable and spot patterns. For example, I noticed that delivery apps were quietly draining my account—small orders adding up to over $100 a month. Eliminating that one habit made a noticeable difference.

Budgeting under pressure isn’t about deprivation—it’s about intentionality. It’s recognizing that temporary sacrifices can prevent long-term damage. For women managing household finances, this level of control can be empowering. It shifts the narrative from helplessness to agency. The goal isn’t to live poorly, but to live wisely, preserving resources until stability returns. And when income does resume, the habits formed during crisis can become the foundation of lasting financial health.

Government and Community Support: Hidden Safety Nets

One of the hardest lessons I learned was that asking for help isn’t weakness—it’s strategy. I had always prided myself on self-reliance, but I realized that refusing available support would only prolong my struggle. I began researching public and nonprofit resources and discovered a network of assistance programs I hadn’t known existed. The first was unemployment insurance. While the application process required documentation and patience, the weekly benefit provided a steady, predictable income stream that supplemented my emergency fund.

Beyond unemployment benefits, I explored food assistance programs. These are designed to help individuals and families maintain nutrition during income loss. I qualified for a local food support service that offered monthly groceries at no cost. It wasn’t charity in the traditional sense—it was a structured system meant to prevent hunger while people regain their footing. I also looked into utility assistance programs, which helped cover a portion of my heating and electricity bills during winter months. These programs aren’t widely advertised, and many people don’t apply due to stigma or misinformation, but they exist for a reason: to keep households stable during transitions.

Local community organizations also played a role. Some offered rental assistance for those at risk of eviction. Others provided free financial counseling, helping me understand my options and avoid costly mistakes. I attended a virtual workshop on debt management and learned how to communicate effectively with creditors. These services were staffed by professionals who had seen similar situations before and could offer practical, nonjudgmental guidance.

The key to accessing these resources is timeliness. Applications can take time to process, so delaying means going without support when it’s needed most. I also learned to keep records of every interaction—dates, names, reference numbers. This helped me follow up efficiently and avoid confusion. For women who often manage both family care and finances, these safety nets can be a lifeline. They aren’t permanent solutions, but they bridge the gap, allowing time to search for work without the constant fear of immediate collapse.

Side Gigs and Quick Income Streams: Beyond Traditional Work

While I searched for full-time employment, I explored ways to generate additional income. I didn’t expect to replace my salary, but even small earnings could extend my financial runway. I started with freelance work using skills I already had—writing, editing, and basic graphic design. Platforms that connect freelancers with short-term projects allowed me to take on assignments that fit my schedule. The pay wasn’t high, but consistency mattered more than size. Completing three small jobs a week added up to a meaningful supplement.

I also considered gig economy opportunities. Delivery services, pet sitting, and local errands were options that required minimal upfront cost. I chose pet sitting because it aligned with my routine and didn’t require a vehicle. Through a reputable platform, I found clients in my neighborhood who needed reliable care for their animals. It wasn’t glamorous, but it was honest work that fit around my job search. The flexibility was crucial—unlike a traditional job, I could adjust hours based on interviews or family needs.

Another avenue was selling unused items. I went through my home and identified clothes, electronics, and household goods I no longer needed. Online marketplaces made it easy to list items with photos and descriptions. The process was slow, but over several weeks, I generated several hundred dollars—enough to cover a month of internet and phone service. I avoided auction sites that charged high fees and focused on local pickup options to reduce hassle.

Not all side gigs are equally viable. Some require investment, others demand too much time for too little return. The key is to focus on low-barrier, reliable options that don’t compromise mental health or job search efforts. For women balancing caregiving and financial responsibility, the ability to earn without rigid schedules is invaluable. These income streams aren’t long-term careers for most, but they serve a critical purpose: maintaining cash flow, preserving savings, and reducing the pressure to accept unsuitable job offers out of desperation.

Managing Debt and Avoiding New Traps

When income drops, debt becomes a major concern. My monthly obligations didn’t disappear, but my ability to meet them did. I knew I had to act proactively. The first step was contacting my creditors—not to avoid payment, but to negotiate. I explained my situation honestly and asked about hardship programs. Many lenders offer temporary forbearance, reduced payment plans, or deferred interest options for those facing unemployment. I was surprised by how willing some were to work with me once I initiated the conversation.

I prioritized debts strategically. High-interest credit card balances were frozen—no new charges, and minimum payments made only when possible. I focused instead on obligations that could lead to immediate consequences if missed: rent, car payments, and utilities. I set up automatic reminders for due dates and used calendar alerts to stay on track. I also avoided taking on new debt at all costs. Payday loans and high-interest personal loans were tempting in moments of stress, but I knew they could trap me in a cycle far worse than the original problem.

Emotional spending was another hidden danger. There were days when I felt defeated, and the urge to buy something—anything—just to feel better was strong. I recognized this as a coping mechanism, not a financial need. To counter it, I developed alternative routines: long walks, journaling, calling a trusted friend. I also unsubscribed from marketing emails that triggered impulse purchases. These small actions helped maintain discipline when willpower was low.

Debt management during unemployment isn’t about elimination—it’s about control. It’s about making informed choices that prevent short-term relief from becoming long-term pain. For women who often carry the emotional weight of family finances, this discipline is both a burden and a strength. By staying calm and strategic, I protected my credit score, avoided collection actions, and preserved my ability to rebuild once the crisis passed.

Rebuilding and Looking Forward: Tools That Last Beyond Crisis

Eventually, I found a new position—one that paid slightly less but offered better stability and growth potential. The job search was exhausting, but the experience transformed my relationship with money. The tools I used to survive unemployment didn’t disappear when my income returned. Instead, they became part of a stronger, more intentional financial life. I kept the crisis budget as a baseline, adjusting it as my income stabilized. I replenished my emergency fund to six months’ worth of essentials, knowing now how quickly life can change.

I continued using the budgeting spreadsheet, refining it to include savings goals and long-term planning. I stayed cautious with credit, paying off balances in full each month. I maintained a side income stream, not out of necessity, but as a buffer against future uncertainty. Most importantly, I developed a habit of regular financial check-ins—monthly reviews of spending, savings, and goals. These small routines created a sense of control that had been missing before the job loss.

The experience also changed my mindset. I no longer saw financial tools as abstract concepts or distant goals. They were practical, necessary, and deeply personal. I began sharing what I’d learned with friends and family, especially other women who managed household budgets. We started a small discussion group focused on financial resilience, where we exchanged tips, resources, and encouragement. It was empowering to turn a difficult experience into something constructive.

Looking back, I wouldn’t wish job loss on anyone. But I can honestly say it made me stronger, wiser, and more prepared. The crisis didn’t just teach me how to survive—it taught me how to build. The same tools that kept me afloat—emergency savings, disciplined budgeting, community support, side income, and debt management—are the same ones that now support my long-term stability. Financial resilience isn’t built in prosperity. It’s forged in difficulty, tested in crisis, and refined through experience. For anyone facing unemployment, the message is clear: you are not alone, and with the right tools, you can not only survive—you can emerge stronger than before.